The CBN AGSMEIS loan offers Nigerian SMEs and agri-businesses up to ₦10 million at a 9% annual interest rate, with a repayment period of up to 7 years. Key steps include mandatory EDI training, a strong business plan, and submission of comprehensive documents via NIRSAL MFB. This guide covers eligibility, application process, required documents, financial specifics, and tips for success for 2024/2025.

The CBN AGSMEIS loan application process for 2024/2025 involves mandatory entrepreneurship training at a CBN-approved Enterprise Development Institute (EDI), followed by the development of a comprehensive business plan. Applicants then submit their application, along with required documents such as CAC registration, BVN, TIN, and valid ID, through the EDI or directly via the NIRSAL Microfinance Bank portal. The loan offers up to ₦10 million at a 9% interest rate with a repayment tenor of up to 7 years, often with a moratorium period. Eligibility requires being an MSME in an eligible sector, a clean credit history, and a certificate of training from an EDI.

Introduction: Unlocking AGSMEIS – Your Gateway to SME Funding in Nigeria

The Central Bank of Nigeria’s Agri-Business/Small and Medium Enterprise Investment Scheme (AGSMEIS) remains one of the most accessible funding options for Nigerian entrepreneurs in 2024/2025. Designed to bridge the critical financing gap faced by MSMEs, this scheme provides low-cost loans with favorable repayment terms to businesses in agriculture, manufacturing, ICT, and other priority sectors. The AGSMEIS loan is a cornerstone of the CBN’s efforts to stimulate economic growth, create jobs, and diversify the Nigerian economy away from oil dependence. It specifically targets the real sector, which has the highest potential for job creation and value addition.

For young entrepreneurs, women-led businesses, and agricultural value chain operators, AGSMEIS represents a rare opportunity to access up to ₦10 million at just 9% interest – significantly lower than commercial bank rates averaging 25-30%. The scheme’s emphasis on capacity building through mandatory entrepreneurship training ensures beneficiaries are better equipped to manage their businesses successfully, thereby increasing their chances of loan repayment and sustainable growth. This focus on capacity building distinguishes AGSMEIS from many other loan schemes, providing not just capital but also essential business knowledge.

This comprehensive guide will walk you through every aspect of the AGSMEIS loan application process, ensuring you have all the information needed for a successful application. We will cover:

- Exact eligibility criteria and sector priorities, detailing who can apply and for what types of businesses.

- Step-by-step application process with current portal links, making it easy to navigate the official channels.

- Required documents (CAC, BVN, TIN etc.), providing a clear checklist to avoid common application errors.

- Financial terms including interest rates and moratorium periods, to help you understand the cost and repayment structure.

- Common reasons for rejection and how to avoid them, offering practical advice to improve your application’s success rate.

- Post-approval best practices, guiding you on how to manage your loan and business effectively after disbursement.

Recent CBN data shows over ₦150 billion disbursed through AGSMEIS since inception, with 60% going to agricultural enterprises. This highlights the scheme’s significant impact on the agricultural sector and its potential to transform small businesses into major contributors to the national economy. With enhanced KYC/AML requirements taking effect in 2026, understanding the complete process is more crucial than ever to ensure compliance and a smooth application journey. The CBN continues to monitor and refine the scheme to ensure its effectiveness and reach.

What is the CBN AGSMEIS Loan Scheme?

The Agri-Business/Small and Medium Enterprise Investment Scheme (AGSMEIS) is a CBN intervention program launched in 2017 to support Nigeria’s real sector development. It is an initiative of the Bankers’ Committee, comprising the CBN and all Deposit Money Banks (DMBs) in Nigeria. The scheme is funded through a 5% deduction from participating banks’ annual profits, demonstrating a collective commitment from the financial sector to foster economic growth. This funding mechanism ensures a sustainable pool of capital for MSMEs. The scheme provides affordable financing to micro, small and medium enterprises (MSMEs) with special focus on agriculture and youth employment, recognizing these as critical drivers of economic diversification and job creation.

Key Features of the AGSMEIS Loan

- Loan Amount: ₦500,000 to ₦10 million depending on business needs and capacity. The amount approved is based on the viability of the business plan and the applicant’s repayment capacity.

- Interest Rate: 9% per annum (flat rate). This is significantly lower than commercial lending rates, making it highly attractive for MSMEs.

- Tenor: Up to 7 years including moratorium period. The extended repayment period eases the burden on new and growing businesses.

- Collateral: Often waived for loans under ₦3 million. For larger amounts, acceptable collateral may include legal mortgages, fixed and floating charges, or other forms of security as determined by NIRSAL MFB.

- Training Requirement: Mandatory entrepreneurship program at CBN-approved EDIs. This ensures beneficiaries acquire essential business management skills.

The AGSMEIS scheme is managed by NIRSAL Microfinance Bank (NMFB), which acts as the primary financial institution for processing applications, disbursing funds, and monitoring repayments. NMFB’s role is crucial in ensuring the scheme’s objectives are met efficiently and transparently.

Target Sectors for AGSMEIS Funding

The scheme prioritizes sectors with high potential for job creation, economic diversification, and value addition. These include:

- Agriculture: This is a primary focus, encompassing crop production (e.g., grains, tubers, fruits), livestock farming (poultry, aquaculture, cattle rearing), fisheries, and agro-processing (value addition to agricultural raw materials).

- Manufacturing: Includes light manufacturing, fabrication, food processing, textiles, garment production, and other small-scale industrial activities.

- Services: Covers a broad range of services such as hospitality (hotels, restaurants), healthcare (clinics, pharmacies), education (private schools, vocational centers), and professional services.

- ICT: Information and Communication Technology, including software development, digital marketing, web design, and IT support services.

- Creative Industries: Fashion design, film production, music production, arts and crafts, and other cultural enterprises that contribute to the creative economy.

- Renewable Energy: Businesses involved in solar panel installation, biomass energy, and other sustainable energy solutions.

Unlike traditional bank loans, AGSMEIS emphasizes business viability over collateral. This approach is designed to empower entrepreneurs who may lack conventional collateral but possess strong business ideas and potential. The mandatory training component ensures borrowers develop essential financial management skills, record-keeping abilities, and strategic planning expertise, reducing default rates which currently stand at just 8% according to NIRSAL MFB data. This low default rate is a testament to the scheme’s robust structure and the effectiveness of the training component.

Who is Eligible for the AGSMEIS Loan? (Detailed Eligibility Criteria)

Understanding the eligibility criteria is the first critical step in securing the AGSMEIS loan. Both personal and business requirements must be met to qualify for this intervention. The CBN and NIRSAL MFB have set clear guidelines to ensure the funds reach deserving and viable enterprises.

Personal Requirements for Applicants

- Nigerian Citizenship: Applicants must be Nigerian citizens, aged between 18 and 65 years. There is a special emphasis and prioritization for youth (18-35 years) and women entrepreneurs.

- Valid BVN and NIN: A Bank Verification Number (BVN) and National Identification Number (NIN) are mandatory. These must be linked to your identity and reflect accurate personal details. Discrepancies can lead to rejection.

- Clean Credit History: Applicants must have a clean credit record, meaning no history of defaulting on previous loans from any financial institution. Credit checks are routinely performed by NIRSAL MFB.

- Tax Identification Number (TIN): Both the individual applicant and the business must possess a valid Tax Identification Number (TIN). This demonstrates tax compliance and formal business operation.

Business Requirements for Applicants

- CAC Registration: The business must be formally registered with the Corporate Affairs Commission (CAC) as either a Business Name or a Limited Liability Company (LTD). Unregistered businesses are not eligible.

- Operational History: For existing businesses, a minimum operational history of at least 6 months is generally required. Start-ups with strong business plans and EDI training are also considered.

- Viable Business Plan: A comprehensive and viable business plan is crucial. It must clearly outline the business model, market analysis, operational strategy, management team, and realistic financial projections. The plan should align with AGSMEIS priority sectors.

- Business Bank Account: The business must operate a dedicated bank account in its registered name. This ensures transparency and proper financial record-keeping.

- Minimum Monthly Turnover: While not a strict universal rule, NIRSAL MFB often looks for a minimum monthly turnover of ₦100,000 for existing businesses, though this can vary by sector and business type.

Mandatory Training Requirement

A non-negotiable requirement for the AGSMEIS loan is the completion of an entrepreneurship development program. You must obtain a certificate from a CBN-approved Enterprise Development Institute (EDI). This training is designed to equip applicants with essential business skills, including:

- Business planning and strategy development.

- Financial management, budgeting, and accounting principles.

- Marketing and sales techniques.

- Record keeping and compliance.

- Risk management and operational efficiency.

The typical cost for this training ranges from ₦5,000 to ₦10,000, depending on the institute and program duration. Some state governments or NGOs may offer subsidies for this training.

Eligible vs. Ineligible Sectors for AGSMEIS

It’s vital to ensure your business falls within the eligible sectors to avoid automatic rejection. The scheme focuses on productive sectors that contribute to economic growth and job creation.

| Eligible Sectors | Ineligible/Low Priority Sectors |

|---|---|

| Crop production (e.g., maize, cassava, rice, vegetables) | Pure trading (buying and selling without significant value addition) |

| Livestock (poultry, fisheries, piggery, cattle rearing) | Importation of finished goods (focus is on local production) |

| Agro-processing (oil milling, packaging, food preservation, juice production) | Gambling/betting services |

| Light manufacturing (textiles, garment making, furniture production, fabrication) | Speculative investments (e.g., real estate speculation) |

| Renewable energy solutions (solar installation, bio-fuel production) | Activities with significant environmental hazards or negative social impact |

| ICT (software development, digital marketing, e-commerce platforms) | Forex trading or cryptocurrency speculation |

| Creative Industries (fashion design, film production, music, arts & crafts) | Multi-level marketing schemes |

| Educational Services (vocational training, private schools) | Businesses involved in illicit activities |

| Healthcare Services (clinics, pharmacies, diagnostic centers) | Businesses with unresolved CBN/NIRSAL loan defaults |

Red Flags for AGSMEIS Applications

Applications from businesses involved in forex trading, multi-level marketing, or with unresolved CBN/NIRSAL loan defaults are automatically rejected. The scheme strongly favors businesses with clear value addition, job creation potential, and a commitment to local content development. Any attempt to misrepresent business activities or provide false information will lead to immediate disqualification and potential legal consequences.

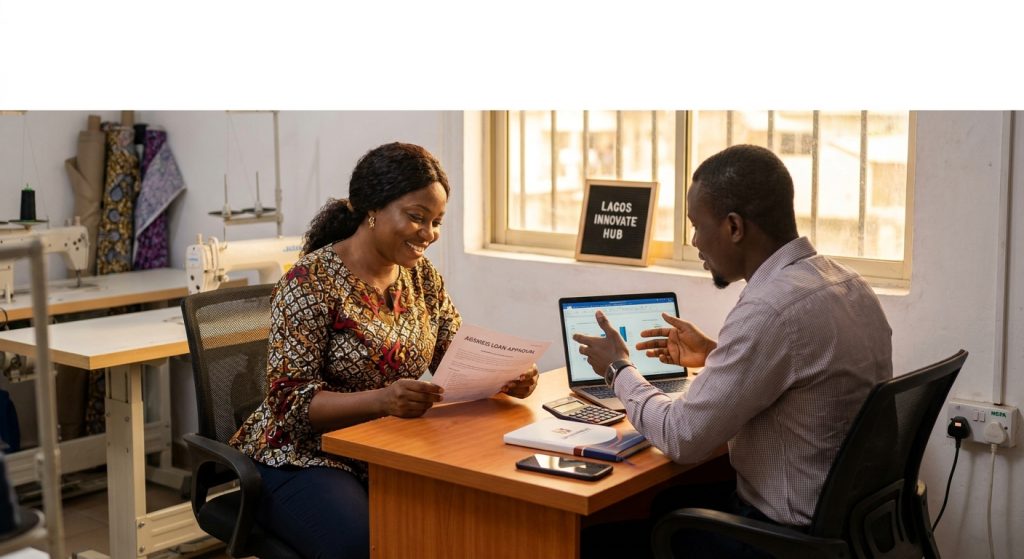

Step-by-Step Guide: How to Apply for the CBN AGSMEIS Loan (2024/2025)

The AGSMEIS loan application process is structured to ensure that only well-prepared and viable businesses receive funding. Following these steps meticulously will significantly increase your chances of approval.

-

Step 1: Attend Mandatory Entrepreneurship Training

This is the foundational step. You cannot apply for the AGSMEIS loan without completing this training. The training equips you with the necessary business acumen to manage your enterprise effectively.

- Locate an EDI: Find a CBN-approved Enterprise Development Institute (EDI) near you. A comprehensive list is available on the NIRSAL MFB’s portal. Popular EDIs include Fate Foundation, BOI Training Centers, and SMEDAN-certified institutes.

- Training Duration: The training typically lasts between 3 to 5 days, depending on the EDI and the program structure. Both physical and virtual (online) options are available, offering flexibility for applicants.

- Cost: The cost for the training generally ranges from ₦5,000 to ₦10,000. Ensure you obtain a certificate of completion, as this is a mandatory document for your application.

-

Step 2: Develop Your Business Plan

Your business plan is the blueprint of your enterprise and a critical component of your loan application. The EDIs provide templates and guidance to help you craft a robust plan.

- Key Sections: Your business plan must include:

- Executive Summary: A concise overview of your business, its mission, and objectives.

- Company Description: Details about your business structure, legal status, and vision.

- Market Analysis: An in-depth analysis of your target market, competition, and marketing strategy.

- Organization and Management: Information about your management team and organizational structure.

- Service or Product Line: Detailed description of what you offer.

- Funding Request: Clearly state the amount of loan requested and how it will be utilized.

- Financial Projections: Realistic 3-year financial forecasts, including profit and loss statements, cash flow projections, and balance sheets.

- Equipment/Input Requirements: A list of essential equipment, raw materials, and other inputs needed for your operations.

- Job Creation Estimates: Project how many direct and indirect jobs your business will create.

-

Step 3: Gather Required Documents

Having all your documents ready and correctly filled out is crucial to avoid delays or rejection. Ensure all documents are clear, legible, and up-to-date.

- Completed EDI training certificate.

- CAC registration documents (Certificate of Incorporation/Business Name Registration, Memorandum and Articles of Association, Form CAC 1.1 or BN 1).

- Valid means of identification (National ID Card, Driver’s License, International Passport, or Voter’s Card).

- BVN (Bank Verification Number) printout from your bank or NIBSS portal.

- TIN (Tax Identification Number) printout for both the individual and the business.

- 6 months business bank statements (for existing businesses).

- Two guarantors (for loans above ₦3 million). Guarantors must have a good credit history and be able to provide their BVN, valid ID, and employment details.

- Passport-sized photographs of the applicant.

- Utility bill (e.g., electricity bill) not older than 3 months, showing your business address.

-

Step 4: Submit Application via NIRSAL MFB

Once you have completed your training and prepared all necessary documents, you can proceed with the application submission.

- Online Portal: The application is primarily submitted online through the official NIRSAL MFB portal: agsmeis.nmfb.com.ng.

- Application Fee: A non-refundable application fee of ₦1,500 is typically required. Be wary of any requests for higher fees from unofficial sources.

- Processing Time: After submission, the initial processing time can range from 4 to 8 weeks. This period involves verification of documents and initial assessment.

- EDI Support: Your EDI can often assist you with the online submission process, ensuring all fields are correctly filled and documents are properly uploaded.

-

Step 5: Loan Assessment & Disbursement

This final stage involves a thorough review of your application and, if approved, the release of funds.

- Physical Verification: NIRSAL MFB officers will conduct physical verification of your business premises and operations to confirm the information provided in your business plan.

- Credit Assessment: A detailed credit assessment will be performed to evaluate your repayment capacity and creditworthiness.

- Approval: If your application passes all checks, it will be approved by the NIRSAL MFB credit committee.

- Disbursement: Funds are typically disbursed directly to equipment vendors or suppliers for capital expenditure, where applicable, to ensure proper utilization. Working capital may be disbursed directly to the business account. The first tranche is often around 70% of the approved amount, with subsequent tranches released based on project milestones.

AGSMEIS Application Timeline Summary

- Training: 1-2 weeks (depending on EDI schedule)

- Document Preparation: 1-2 weeks (gathering and organizing all required paperwork)

- Application Processing: 4-8 weeks (from online submission to initial assessment)

- Disbursement: 2-4 weeks after final approval (can vary based on verification and vendor payments)

Financial Terms & Repayment Structure

Understanding the financial terms of the AGSMEIS loan is crucial for effective financial planning and successful repayment. The scheme is designed to be affordable and flexible for MSMEs.

Loan Amounts by Business Type

The maximum loan amount an applicant can receive depends on the classification of their business and the viability of their project:

- Micro Enterprises: Typically eligible for loans ranging from ₦500,000 to ₦1 million. These are often small businesses with limited capital requirements.

- Small Businesses: Can access loans between ₦1 million and ₦5 million. These businesses usually have a slightly larger operational scale and higher capital needs.

- Medium Enterprises: Eligible for loans from ₦5 million up to the maximum of ₦10 million. These are businesses with significant growth potential and substantial capital investment requirements.

Interest Rate and Calculation Example

The AGSMEIS loan comes with a highly competitive interest rate of 9% per annum, calculated on a flat rate basis. This means the interest is calculated on the initial principal amount for the entire loan tenor.

Interest Calculation Example:

Let’s consider a loan of ₦3 million at 9% interest over 5 years (60 months):

- Annual Interest: 9% of ₦3,000,000 = ₦270,000

- Total Interest over 5 years: ₦270,000 x 5 years = ₦1,350,000

- Total Amount to Repay (Principal + Interest): ₦3,000,000 + ₦1,350,000 = ₦4,350,000

- Monthly Repayment: ₦4,350,000 / 60 months = ₦72,500

This example illustrates the affordability of the AGSMEIS loan compared to commercial rates.

Moratorium Periods

A moratorium period is a grace period during which the borrower is not required to make principal or interest payments. This is particularly beneficial for businesses with long gestation periods, allowing them to stabilize operations before commencing full repayments.

- Agriculture: Typically enjoys the longest moratorium period due to the seasonal nature of farming. This can be up to 18 months for principal repayment and 6 months for interest payments.

- Manufacturing: Usually receives a moratorium of up to 12 months for principal repayment and 3 months for interest payments.

- Services: May have a shorter moratorium, often up to 6 months for principal repayment, with interest payments commencing earlier or immediately.

The specific moratorium period for your loan will be clearly stated in your loan offer letter from NIRSAL MFB.

Repayment Options and Penalties

NIRSAL MFB offers various convenient repayment options to facilitate timely payments:

- Direct Debit: An automated system where repayments are directly debited from your business bank account on scheduled dates. This is the most common and recommended method.

- Standing Payment Order: You can set up a standing order with your bank to transfer the monthly repayment amount to NIRSAL MFB.

- Mobile Money Transfers: Some USSD codes and mobile banking platforms may be integrated for easier repayments.

- Over-the-Counter Payments: Payments can also be made at designated NIRSAL MFB branches or partner banks.

Late Payment Penalties:

It is crucial to adhere to the repayment schedule. Late payments attract penalties, typically a 1% monthly charge on overdue amounts. Consistent defaults can lead to:

- Negative impact on your credit score, making it difficult to access future loans.

- Possible blacklisting from future CBN intervention schemes.

- Legal action by NIRSAL MFB to recover the outstanding debt.

If you anticipate difficulties in meeting your repayment obligations, it is advisable to communicate proactively with NIRSAL MFB to explore potential restructuring options.

Common Reasons for Rejection & How to Avoid Them

While the AGSMEIS loan is designed to be accessible, a significant number of applications are rejected due to preventable errors. Understanding these common pitfalls can help you prepare a stronger application.

Top 5 Reasons for AGSMEIS Loan Rejection

-

Incomplete Documentation (32% of cases): This is the most frequent reason for rejection. Missing documents, expired IDs, unclear scans, or inconsistent information across different documents are common issues.

- Solution: Use the NIRSAL MFB checklist provided during your EDI training. Double-check every required document before submission. Ensure all uploads are clear, legible, and current. Consider having your EDI mentor review your documents before final submission.

-

Weak Business Plan (28%): A poorly articulated business plan that lacks realism, clear financial projections, or a viable market strategy will likely be rejected. Ambiguous objectives, unrealistic revenue forecasts, or a lack of understanding of the target market are red flags.

- Solution: Invest significant time in developing a comprehensive and realistic business plan. Seek guidance from your EDI trainers, who are experts in this area. Ensure your financial projections are well-researched and justifiable. Clearly articulate your unique selling proposition and how your business will generate revenue and create jobs.

-

BVN/TIN Mismatch (19%): Discrepancies between the names, dates of birth, or other details on your BVN, TIN, and other identification documents (like your National ID or CAC registration) can lead to immediate rejection.

- Solution: Before applying, verify your details on the FIRS TIN checker and the NIBSS BVN portal. Ensure all your official documents reflect consistent information. If there are discrepancies, get them rectified with the relevant authorities (e.g., your bank for BVN, FIRS for TIN, NIMC for NIN) before applying.

-

Sector Ineligibility (12%): Applying for a business that falls outside the priority sectors or is explicitly listed as ineligible will result in rejection.

- Solution: Carefully review the list of eligible and ineligible sectors provided in Section 3 of this guide. If your business is in a borderline sector, consult with your EDI or NIRSAL MFB representatives before investing time and resources in the application. Focus on how your business adds value and creates jobs within the approved sectors.

-

Previous Loan Default (9%): A history of defaulting on previous loans, whether from commercial banks, microfinance institutions, or other government intervention schemes, will disqualify you.

- Solution: Ensure you have a clean credit history. If you have outstanding debts or a history of default, it is imperative to clear them and obtain a clearance certificate before applying for AGSMEIS. NIRSAL MFB conducts thorough credit checks with credit bureaus.

Appeal Process for Rejected Applicants

If your AGSMEIS application is rejected, you typically have an opportunity to appeal the decision. Rejected applicants can request a review within 14 days of receiving the rejection notification. This appeal should be submitted via the NIRSAL MFB portal, providing additional documentation or clarification to address the specific reason for rejection. It is crucial to understand the exact reason for rejection to effectively address it in your appeal. Your EDI can also provide guidance during the appeal process.

Alternatives to AGSMEIS (Comparison Table)

While AGSMEIS is an excellent option, it’s beneficial for Nigerian entrepreneurs to be aware of other funding opportunities available for MSMEs. Each scheme has its unique features, eligibility criteria, and focus areas. This comparison table highlights some prominent alternatives.

| Scheme | Max Amount | Interest Rate | Tenor | Collateral Requirements | Training Required | Key Focus/Target |

|---|---|---|---|---|---|---|

| AGSMEIS (CBN) | ₦10 million | 9% p.a. (flat) | Up to 7 years | Often waived for <₦3m; otherwise, flexible | Yes (EDI) | Agri-business, MSMEs, youth, job creation |

| BOI Youth Entrepreneurship Support Programme (YES-P) | ₦3 million | 5% p.a. | Up to 3 years | Guarantors, business assets | Yes (BOI-certified training) | Young entrepreneurs (18-35), innovation, manufacturing |

| SMEDAN Conditional Grant Scheme (CGS) | ₦1 million | 9% p.a. | Up to 5 years | None (grant component) | No (but business development services provided) | Micro-enterprises, informal sector formalization |

| Lagos State Employment Trust Fund (LSETF) Loan | ₦5 million | 12% p.a. | Up to 3 years | Business assets, guarantors | Yes (LSETF-approved training) | Lagos-based MSMEs, job creation in Lagos |

| NIRSAL MFB CBN Anchor Borrowers’ Programme (ABP) | ₦25 million (for large farmers/cooperatives) | 5% p.a. | Up to 7 years (crop cycle dependent) | Fixed assets, off-taker agreement | No (but technical support provided) | Agricultural value chain, food security |

| Development Bank of Nigeria (DBN) Loans | Varies (up to ₦200 million via PFIs) | Market-driven (lower than commercial) | Up to 10 years | Determined by PFI | No (but capacity building for PFIs) | MSMEs, on-lending through commercial banks/MFBs |

| Bank of Agriculture (BOA) Loans | Varies (up to ₦50 million) | 5-15% p.a. | Up to 10 years | Land, equipment, guarantors | No (but agricultural extension services) | Agricultural sector, rural development |

Choosing the Right Funding Option

When considering alternatives, evaluate them based on:

- Eligibility: Do you meet the specific criteria for the scheme?

- Loan Amount: Does the maximum amount meet your business needs?

- Interest Rate & Tenor: Are the repayment terms favorable and sustainable for your business?

- Collateral: What are the collateral requirements, and can you meet them?

- Training/Support: Does the scheme offer valuable capacity building or technical support?

- Geographic Focus: Is the scheme specific to a particular state or region?

Diversifying your knowledge of available funding options can significantly enhance your chances of securing capital for your business growth.

FAQs: People Also Ask

Q: Can I get AGSMEIS loan without CAC registration?

A: No, CAC registration (either Business Name or Limited Company) is a mandatory requirement for the AGSMEIS loan. The scheme is designed to support formal businesses. If your business is currently registered as a Business Name and you are applying for amounts above ₦3 million, it is advisable to consider upgrading to a Limited Liability Company (LTD) as it often provides more credibility and legal structure for larger loans.

Q: How long does approval take in 2024?

A: The current processing time for AGSMEIS loan approval in 2024 typically ranges from 6 to 10 weeks from the date of complete application submission. This timeline includes document verification, physical business assessment, and credit committee review. It’s important to note that agricultural projects often receive priority processing due to the scheme’s strong focus on the agricultural sector and its seasonal nature.

Q: Can civil servants apply?

A: Yes, civil servants can apply for the AGSMEIS loan, but with specific conditions. The business must be registered as a side venture and must not conflict with public service rules or your primary employment. You must demonstrate that the business is genuinely operational and managed, and that your involvement does not compromise your official duties. Full disclosure of your employment status is required during the application process.

Q: Is there any age limit?

A: The AGSMEIS loan is open to Nigerian citizens aged between 18 and 65 years. However, applicants aged 18-35 years (youth) receive additional scoring advantages and are often prioritized, aligning with the CBN’s youth empowerment initiatives. This prioritization reflects the scheme’s goal of fostering entrepreneurship among the younger demographic.

Q: Can the loan be used to buy land?

A: No, the AGSMEIS loan is strictly designed to fund productive assets, working capital, and operational expenses that directly contribute to business growth and job creation. It cannot be used for the purchase of land or real estate speculation. Funds are typically disbursed for items like equipment, machinery, raw materials, inventory, and operational costs. This ensures the loan directly impacts the productive capacity of the business.

Q: What if my business is a startup?

A: AGSMEIS supports both existing businesses and viable startups. For startups, a strong, well-researched business plan is even more critical, demonstrating market potential, clear operational strategies, and realistic financial projections. The mandatory EDI training is particularly beneficial for startups, providing foundational knowledge and guidance in developing their business model.

Q: Do I need a guarantor for all loan amounts?

A: For AGSMEIS loans below ₦3 million, collateral requirements are often waived, and a guarantor might not be strictly necessary. However, for loans above ₦3 million, NIRSAL MFB typically requires two guarantors. These guarantors must have a clean credit history, verifiable income, and be able to provide their BVN, valid ID, and employment details. The specific requirements will be communicated during the application process.

Q: Can I apply if I have an existing loan?

A: Yes, you can apply for the AGSMEIS loan even if you have an existing loan, provided your credit history is clean and you are not in default on any existing facility. NIRSAL MFB will assess your overall debt burden and repayment capacity to determine if you can comfortably service an additional loan. Having a good repayment record on existing loans can actually strengthen your application.

Red Flags: What to Watch Out For

Navigating the AGSMEIS application process requires vigilance to avoid scams and common pitfalls. Being aware of these red flags can protect you from fraudulent activities and ensure a smooth application journey.

Key Red Flags and How to Avoid Them

-

Fake EDI Scams: There have been instances of fraudulent organizations posing as CBN-approved Enterprise Development Institutes. These fake EDIs may charge exorbitant fees for training or promise guaranteed loan approvals.

- Solution: Always verify the legitimacy of any EDI before making payments or attending training. Use only the official list of CBN-approved EDIs available on the NIRSAL MFB’s official website. If an EDI is not on this list, it is likely a scam.

-

Advance Fee Fraud: Be extremely cautious of individuals or groups who ask for “processing fees,” “facilitation fees,” or “guaranteed approval fees” beyond the official ₦1,500 application charge. Legitimate AGSMEIS processes do not involve such payments to individuals.

- Solution: Never pay money to any individual claiming to be an AGSMEIS agent or NIRSAL MFB staff promising to fast-track your loan. All official payments are made directly to NIRSAL MFB through designated channels. Report any such requests to NIRSAL MFB or the CBN.

-

Loan App Harassment and Illegal Lenders: The Federal Competition and Consumer Protection Commission (FCCPC) has been actively cracking down on illegal loan apps in Nigeria, banning 37 in 2024 due to predatory practices and harassment. Do not confuse these with legitimate intervention schemes.

- Solution: Only use NIRSAL MFB’s official channels (agsmeis.nmfb.com.ng) for your AGSMEIS application. Avoid engaging with unverified online platforms or mobile applications that promise quick loans without proper due diligence.

-

Guarantor Requirements Misinformation: For loans above ₦3 million, guarantors are typically required. Be wary of individuals who claim you don’t need guarantors for larger amounts or offer to provide fake guarantors for a fee.

- Solution: Ensure your chosen guarantors have clean credit histories and are fully aware of their responsibilities. Providing false guarantor information can lead to immediate disqualification and legal repercussions for all parties involved.

-

Disbursement Delays and Lack of Communication: While some delays can occur due to high application volumes, prolonged silence or inability to get updates after approval can be a red flag.

- Solution: After approval, maintain regular, professional follow-up with your assigned NIRSAL MFB relationship officer or the EDI that facilitated your application. Keep records of all communications. If you experience unusual delays or lack of response, escalate your concerns through official NIRSAL MFB customer service channels.

-

Promises of ‘Guaranteed’ Approval: No legitimate loan scheme can guarantee approval. The approval process is based on strict eligibility criteria, business viability, and credit assessment.

- Solution: Be skeptical of anyone who promises guaranteed approval, especially if they ask for money upfront. Focus on preparing a strong, compliant application rather than seeking shortcuts.

What to Do This Week: Your 5-Point Checklist

To maximize your chances of securing the CBN AGSMEIS loan, proactive preparation is key. Here’s a practical checklist of actions you can take this week to get started or advance your application.

-

Verify Your CAC Status

Ensure your business registration is current and accurate. This is a fundamental requirement for AGSMEIS.

- Action: Visit the Corporate Affairs Commission (CAC) portal to confirm your business registration details.

- Consideration: If your business is currently registered as a Business Name (BN) and you plan to apply for a loan above ₦3 million, consider upgrading to a Limited Liability Company (LTD). This often adds credibility and is sometimes preferred for larger funding amounts.

-

Pull Your Credit Report

Understanding your credit standing is vital, as a clean credit history is a non-negotiable eligibility criterion.

- Action: Obtain a free credit report from a licensed credit bureau in Nigeria, such as CRC Credit Bureau or FirstCentral Credit Bureau.

- Benefit: This allows you to identify any potential red flags, errors, or outstanding debts that could hinder your application. Address any issues proactively before applying.

-

Register for EDI Training

The mandatory entrepreneurship training is the gateway to the AGSMEIS loan. Don’t delay this crucial step.

- Action: Visit the NIRSAL MFB EDI listing to find an approved training center nearest to you. Contact them to inquire about their next training schedule and registration process.

- Tip: Book your spot as soon as possible, as training slots can fill up quickly, especially in popular locations.

-

Open a Dedicated Business Account

Having a separate bank account for your business is essential for financial transparency and is a requirement for the loan.

- Action: Visit any NIRSAL-partnered commercial bank (e.g., Access Bank, Zenith Bank, UBA, First Bank) with your CAC registration documents to open a dedicated business account.

- Importance: This demonstrates financial discipline and allows NIRSAL MFB to easily track your business transactions and assess your financial health.

-

Prepare Your Tax Documents

A valid Tax Identification Number (TIN) for both you and your business is mandatory for compliance.

- Action: If you or your business do not yet have a TIN, register for one via the FIRS eTax portal. If you have one, ensure it is active and linked to your correct details.

- Compliance: This step ensures you meet the tax compliance requirements set by the CBN and NIRSAL MFB, which are increasingly stringent.

By systematically addressing these steps, you’ll position yourself for AGSMEIS success in the 2024/2025 application cycle. Remember – the early applicants typically have higher approval rates before quarterly disbursement quotas are met. Proactive preparation and timely submission are your best allies in securing this valuable funding for your Nigerian business.