Quick Summary

Understanding your credit score is crucial for financial success in Nigeria. This comprehensive guide, updated for 2026, demystifies credit scores, explains how they’re calculated by bureaus like CRC Credit Bureau, FirstCentral Credit Bureau, and CreditRegistry, and provides actionable steps to improve yours. Learn how to check your score for free, interpret your credit report, and leverage a strong credit history to secure better loan approvals from banks, MFIs, and fintech lenders across Nigeria.

Quick Answer

A credit score in Nigeria is a numerical representation of your creditworthiness, primarily generated by credit bureaus (CRC Credit Bureau, FirstCentral Credit Bureau, CreditRegistry) based on your borrowing and repayment history. Lenders use this score to assess your risk before approving loans. To improve it, consistently pay debts on time, manage your credit utilization, and regularly check your credit report for accuracy.

1. Introduction: Understanding Your Financial Footprint in Nigeria

In today’s Nigeria, your financial footprint extends far beyond the balance in your bank account. It encompasses your credit score – a single, powerful number that can open or close doors to crucial financial opportunities. As of 2026, understanding and managing your credit score is no longer just for the financially savvy; it’s a fundamental skill for every Nigerian looking to borrow money, whether for a personal loan, a business venture, or even asset financing.

A strong credit score can mean the difference between getting approved for a loan at a favourable interest rate and being rejected outright or offered terms that are simply unaffordable. It impacts your ability to secure mortgages, access vehicle financing, and even influences some landlords and employers who are increasingly using credit checks as part of their assessment processes. This guide will walk you through everything you need to know about credit scores in Nigeria, helping you take control of your financial future.

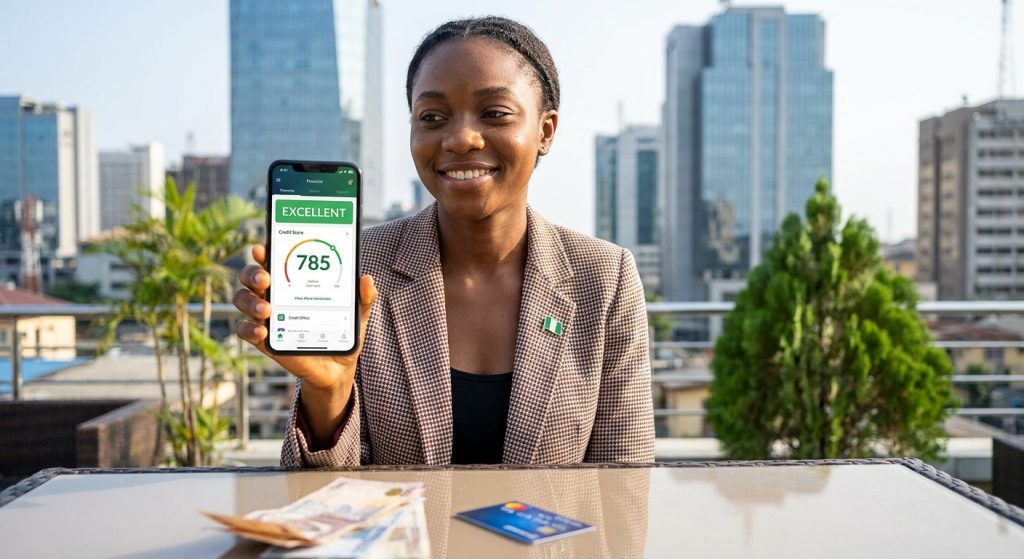

2. What is a Credit Score and How Does it Work in Nigeria?

Simply put, a credit score is a three-digit number that tells lenders how likely you are to repay your debts. It’s like a financial report card, summarizing your past borrowing behaviour. The higher your score, the lower your perceived risk to lenders, and the more likely you are to get approved for credit products.

In Nigeria, credit scores are primarily generated by three major credit bureaus:

- CRC Credit Bureau

- FirstCentral Credit Bureau

- CreditRegistry

These bureaus are regulated by the Central Bank of Nigeria (CBN) and act as central repositories for credit information. They collect data from various financial institutions – including commercial banks, microfinance banks, finance companies, and even some fintech lenders – about your borrowing and repayment activities. This data includes details of loans you’ve taken, how consistently you’ve paid them back, and your current debt obligations.

When you apply for a loan, the lender requests your credit report and score from one or more of these bureaus. The bureau then processes the collected data using complex algorithms to produce your credit score. This score helps the lender quickly assess your creditworthiness and make an informed decision about your loan application.

3. The Key Factors That Influence Your Nigerian Credit Score

Your credit score isn’t just a random number; it’s a dynamic reflection of several key aspects of your financial behaviour. While the exact weighting might vary slightly between the different credit bureaus in Nigeria, the underlying principles are consistent with global best practices. Here are the most crucial factors:

- Payment History (Approx. 35%): This is by far the most important factor. Consistently paying your loans, credit card bills, and other financial commitments on time demonstrates reliability. Even a single late payment can negatively impact your score, especially if it’s recent. Missing payments, defaulting on loans, or having accounts sent to collections will severely damage your score.

- Amounts Owed (Credit Utilization) (Approx. 30%): This refers to the amount of debt you currently have compared to your total available credit. For instance, if you have a credit limit of ₦100,000 and you’ve used ₦80,000, your credit utilization is 80%. A high utilization ratio suggests you might be over-reliant on credit and could struggle to repay new debts. Aim to keep your credit utilization below 30%.

- Length of Credit History (Approx. 15%): The longer you’ve responsibly managed credit, the better. A long history of on-time payments shows a proven track record. If you’re new to credit, your score might be lower simply due to a lack of data. This is why it’s often advised to start building credit early, even with small, manageable loans.

- New Credit (Approx. 10%): This factor considers how many new credit accounts you’ve opened recently and how many credit inquiries have been made on your report. Opening too many new accounts in a short period can signal higher risk to lenders, as it might suggest financial distress or an inability to manage existing debts. Each time a lender checks your credit for a loan application (a “hard inquiry”), it can slightly lower your score temporarily.

- Credit Mix (Approx. 10%): Having a healthy mix of different types of credit (e.g., a personal loan, an asset finance loan, a small business loan) can positively impact your score. It shows you can responsibly manage various forms of debt. However, only take on credit you genuinely need and can afford.

- Nigerian-Specific Considerations:

- BVN and NIN Linkage: Your Bank Verification Number (BVN) and National Identity Number (NIN) are crucial for identifying you across the financial system. Ensure all your financial accounts are properly linked to these identifiers to ensure all your credit activities are accurately reported under your profile.

- Digital Footprint: With the rise of fintechs, consistent payment of utility bills (electricity, internet, cable TV) through digital platforms can indirectly contribute to a positive digital footprint, which some innovative lenders might consider, especially for those with thin credit files. While not directly part of the traditional credit score calculation, it builds a picture of financial responsibility.

4. How to Check Your Credit Score in Nigeria: A Step-by-Step Guide

Regularly checking your credit score and report is a smart financial habit. It allows you to monitor your financial health, detect potential identity theft or errors, and understand where you stand before applying for new credit. The good news is that, as mandated by CBN regulations, every Nigerian consumer is entitled to one free credit report annually from each of the credit bureaus.

Here’s how to get yours in 2026:

Required Documents for All Bureaus:

Before you start, ensure you have the following ready:

- Your Bank Verification Number (BVN)

- Your National Identity Number (NIN)

- A valid means of identification (e.g., National ID Card, Driver’s License, International Passport, Voter’s Card)

- Your full name, date of birth, and current address.

A. Checking Your Credit Score with CRC Credit Bureau

CRC Credit Bureau is one of Nigeria’s leading credit reporting agencies.

Online Portal (Recommended for speed):

- Visit the Website: Go to www.crccreditbureau.com.

- Register/Login: If you’re a new user, click on “Get Your Credit Report” or “Register.” You’ll need to provide your personal details, BVN, and create a password. If you’re a returning user, simply log in.

- Request Report: Navigate to the section for requesting your credit report. You’ll typically see an option for a “Free Annual Credit Report.”

- Verify Identity: You might be asked to answer some security questions or input an OTP sent to your registered phone number or email to verify your identity.

- View/Download: Once verified, your credit report and score should be displayed instantly or available for download as a PDF.

Mobile App:

- Download App: Search for “CRC Credit Bureau” on the Google Play Store or Apple App Store.

- Register/Login: Follow the in-app instructions to register or log in using your existing CRC credentials.

- Request Report: Locate the option to request your credit report.

- View/Download: Your report will be accessible within the app.

Email Request:

- Compose Email: Send an email to a designated address (often provided on their website, e.g., [email protected]).

- Attach Documents: Attach scanned copies of your valid ID, and clearly state your full name, BVN, NIN, date of birth, and request for your free annual credit report.

- Timeline: Expect a response and your report within 2-5 business days.

Physical Office:

- Visit Office: Go to CRC Credit Bureau’s office (check their website for current addresses, e.g., in Lagos or Abuja).

- Fill Form: Request and fill out a credit report request form.

- Submit Documents: Present your valid ID, BVN, and NIN.

- Timeline: You might receive your report on the spot or be asked to return later.

B. Checking Your Credit Score with FirstCentral Credit Bureau

FirstCentral Credit Bureau also offers convenient ways to access your credit information.

Online Portal:

- Visit the Website: Go to www.firstcentralcreditbureau.com.

- Register/Login: Click on “Get Your Credit Report” or “Consumer Portal.” Register if you’re new, providing your details, BVN, and creating an account.

- Request Report: Select the option for your free annual credit report.

- Verify Identity: Complete any identity verification steps.

- View/Download: Your report should be available instantly or sent to your registered email address.

Email Request:

- Compose Email: Send an email to their consumer support address (e.g., [email protected]).

- Attach Documents: Attach scanned copies of your valid ID, and clearly state your full name, BVN, NIN, date of birth, and request for your free annual credit report.

- Timeline: Expect your report via email within 2-5 business days.

C. Checking Your Credit Score with CreditRegistry

CreditRegistry is another key player in Nigeria’s credit reporting landscape.

Online Portal:

- Visit the Website: Go to www.creditregistry.ng.

- Register/Login: Look for “Get Your Credit Report” or “Individual Login.” Register your details, BVN, and set up your account.

- Request Report: Choose the option for your free annual credit report.

- Verify Identity: Follow the on-screen prompts for identity verification.

- View/Download: Your report should be available for immediate access or download.

Mobile App:

- Download App: Search for “CreditRegistry” on your app store.

- Register/Login: Create an account or log in.

- Request Report: Navigate to the credit report section.

- View/Download: Access your report directly from the app.

Naira Pricing for Additional Reports (Beyond the Free One):

While you get one free report annually from each bureau, if you need more frequent checks, you will incur a fee. As of 2026, the typical range for an additional credit report from any of these bureaus is ₦1,500 – ₦2,500 per report. These prices may see slight adjustments due to inflation, but they remain relatively affordable for monitoring your credit health.

5. Understanding Your Credit Report: What to Look For

Receiving your credit report can feel overwhelming, but it’s a treasure trove of information about your financial history. Don’t just glance at your score; delve into the details. Here’s what to pay close attention to:

- Personal Information: Double-check your name, address, date of birth, BVN, and NIN. Any inaccuracies here could lead to your credit history being mixed up with someone else’s or make it difficult for lenders to verify your identity.

- Credit Accounts: This section lists all your loans, credit cards, and other credit facilities. Verify that:

- All accounts listed belong to you.

- The account numbers and lender names are correct.

- The current status (open, closed, active, defaulted) is accurate.

- The outstanding balances match your records.

- Payment History: This is a detailed month-by-month record of your payments for each account. Look for:

- Any late payments you don’t recall.

- Accounts marked as “defaulted” or “written off” if you believe they were paid.

- Consistent on-time payments should be clearly reflected.

- Inquiries: This section shows who has accessed your credit report.

- Hard Inquiries: These occur when you apply for a loan or credit. Too many hard inquiries in a short period can negatively impact your score.

- Soft Inquiries: These are usually initiated by you (when checking your own report) or by lenders for pre-approval offers. They do not affect your score.

- Look for any hard inquiries you don’t recognize, which could indicate fraudulent activity.

- Public Records (Less Common but Possible): While not as prevalent in Nigerian credit reports as in some other countries, this section would list information from public sources, such as court judgments or bankruptcies. If anything appears here, ensure its accuracy.

How to Spot Errors and Discrepancies:

It’s crucial to review your report meticulously. Look for:

- Accounts you never opened.

- Incorrect payment statuses (e.g., an account you paid on time being marked as late).

- Wrong outstanding balances.

- Duplicate accounts.

- Incorrect personal information.

If you find any errors, you have the right to dispute them with the credit bureau. They are legally obligated to investigate and correct inaccuracies within a specified timeframe (typically 30 days).

6. Boosting Your Credit Score in Nigeria: Practical Strategies for Loan Approval

A good credit score is your passport to better financial opportunities. Here are actionable strategies to improve and maintain a healthy credit score in Nigeria:

- Pay Bills On Time, Every Time: This is the golden rule. Set up reminders, automate payments where possible, or mark due dates on your calendar. This includes all forms of credit – personal loans, business loans, asset finance, and even utility bills if they are reported to bureaus (though less common for direct score impact, it builds a positive financial behaviour).

- Keep Credit Utilization Low: Aim to use no more than 30% of your available credit limit. If you have a ₦100,000 credit limit, try to keep your outstanding balance below ₦30,000. Paying down existing debts is more impactful than opening new credit lines.

- Limit New Credit Applications: Only apply for credit when you genuinely need it. Each “hard inquiry” can slightly ding your score. Space out your applications.

- Maintain a Mix of Credit (Responsibly): Once you have a strong foundation, having a mix of different credit types (e.g., a small personal loan and a hire purchase agreement) can show you can manage various debts. However, never take on debt you don’t need just to improve your mix.

- Avoid Closing Old Accounts (Especially if in Good Standing): Older accounts with a good payment history contribute positively to your “length of credit history.” Closing them might shorten your average credit age.

- Monitor Your Credit Report Regularly: As discussed, check your free annual report from each bureau. This helps you catch errors and identify areas for improvement.

- Dispute Errors Promptly: If you find inaccuracies, contact the credit bureau immediately with supporting documentation. Correcting errors can significantly boost your score.

- Start Small and Build: If you have no credit history (a “thin file”), consider taking out a small, manageable loan from a reputable MFI or fintech that reports to credit bureaus. Pay it back diligently to start building your history. Examples include Carbon (formerly Paylater), Renmoney, or even small co-operative loans.

- Secure Loans with Collateral (If Necessary): If your score is low, some lenders might offer secured loans (e.g., against a car or property). While this is a riskier option if you default, successfully repaying a secured loan can help rebuild your credit.

- Consolidate Debt (Carefully): If you have multiple high-interest debts, a debt consolidation loan could simplify payments and potentially lower your overall interest. However, ensure the new loan doesn’t increase your total debt or extend your repayment period excessively.

7. The Impact of Your Credit Score on Loan Approval in Nigeria

Your credit score is the first impression you make on a lender. Here’s how it directly influences your loan applications:

- Approval or Rejection:

- High Score (e.g., 700+): You are seen as a low-risk borrower. Lenders are more likely to approve your loan application.

- Average Score (e.g., 600-699): Approval is possible, but you might face stricter terms or higher interest rates.

- Low Score (e.g., below 600): You are considered a high-risk borrower. Loan applications are often rejected, or you might only qualify for very small loans with extremely high interest rates from specific lenders.

- Interest Rates: A strong credit score qualifies you for lower interest rates. Lenders compete for low-risk borrowers, offering them more attractive terms. A lower interest rate means you pay less over the life of the loan. For example, a bank might offer a prime borrower an unsecured personal loan at 20% per annum, while a borrower with a poor score might be offered a similar loan from a fintech at 5% per month (60% per annum) or more.

- Loan Amount and Tenor: Lenders are more comfortable offering larger loan amounts and longer repayment periods (tenors) to borrowers with excellent credit scores. This gives you more flexibility and access to the funds you need.

- Collateral Requirements: With a good credit score, you might qualify for unsecured loans (loans without collateral). If your score is low, lenders will almost certainly demand collateral (e.g., property, vehicle, or a guarantor) to mitigate their risk.

- Processing Time: Loan applications from borrowers with high credit scores are often processed faster, as lenders spend less time on manual risk assessment.

Comparative Table: Impact of Credit Score on Loan Terms

| Feature | Excellent Credit Score (700-850) | Good Credit Score (650-699) | Fair Credit Score (600-649) | Poor Credit Score (300-599) |

|---|---|---|---|---|

| Approval Chance | Very High | High | Moderate | Low to Very Low |

| Interest Rates | Best rates (e.g., 18-25% p.a. for unsecured personal loans) | Good rates (e.g., 25-35% p.a.) | Higher rates (e.g., 35-60% p.a.) | Very high rates (e.g., 60-120% p.a. or even higher from some fintechs) |

| Loan Amount | Higher amounts, greater flexibility | Good amounts | Limited amounts | Very small amounts, if any |

| Tenor (Repayment) | Longer repayment periods available | Standard repayment periods | Shorter repayment periods | Very short repayment periods |

| Collateral | Often unsecured | May be unsecured or require minimal collateral | Often requires collateral or a guarantor | Almost always requires collateral or a guarantor |

| Processing Time | Fastest | Fast | Standard | Longer, more scrutiny |

| Example Lenders | Major Commercial Banks (GTBank, Zenith, Access), Tier 1 MFIs | Tier 1/2 Commercial Banks, Reputable MFIs, some Fintechs | Some MFIs, newer Fintechs, specific loan products | Predatory Lenders, some quick loan apps (use with caution) |

8. Common Misconceptions About Credit Scores in Nigeria

Let’s clear up some common misunderstandings about credit scores:

- “My BVN is enough to get a loan.” While your BVN is essential for identification, it doesn’t guarantee a loan. Lenders still need to assess your repayment capacity, which is where your credit score comes in.

- “Checking my own credit report hurts my score.” No, it doesn’t. Checking your own report is a “soft inquiry” and has no impact on your score. Only “hard inquiries” from lenders when you apply for credit affect your score.

- “I don’t borrow, so I have a perfect credit score.” Not true. If you’ve never borrowed, you have no credit history, often referred to as a “thin file.” Lenders have no data to assess your risk, which can make it difficult to get approved for loans. You need to build credit responsibly.

- “Once my score is bad, it’s bad forever.” Absolutely not. While negative marks stay on your report for a few years (typically 3-5 years for defaults in Nigeria), consistent positive behaviour (on-time payments, reducing debt) will gradually improve your score over time.

- “All credit bureaus have the same score.” While they use similar data, each bureau has its own proprietary scoring model. Your score might vary slightly between CRC, FirstCentral, and CreditRegistry. It’s advisable to check all three.

- “My income determines my credit score.” Your income influences how much you can afford to borrow, but it doesn’t directly factor into your credit score calculation. The score is about your repayment behaviour, not your earnings.

9. Regulatory Landscape and Consumer Protection (CBN)

The Central Bank of Nigeria (CBN) plays a critical role in regulating the credit reporting industry and protecting consumers. Key aspects include:

- Mandate for Credit Bureaus: The CBN licenses and supervises the operations of credit bureaus in Nigeria, ensuring they operate fairly and transparently.

- Right to Free Annual Report: As highlighted, CBN regulations stipulate that every individual has the right to one free credit report from each credit bureau annually. This empowers consumers to monitor their financial health.

- Dispute Resolution: The CBN ensures that credit bureaus have clear processes for consumers to dispute inaccuracies on their credit reports. If a dispute is not resolved satisfactorily by the bureau, consumers can escalate their complaints to the CBN’s Consumer Protection Department.

- Data Privacy: The CBN, in collaboration with other regulatory bodies like NITDA, ensures that credit bureaus handle consumer data with strict privacy and security protocols, in line with the Nigeria Data Protection Regulation (NDPR) 2026 and other relevant laws.

These regulations provide a framework that protects consumers and promotes a fair and efficient credit market in Nigeria.

10. The Future of Credit Scoring in Nigeria

The Nigerian credit landscape is rapidly evolving. Here’s what we can expect:

- Increased Data Sources: Beyond traditional loans, more alternative data sources will likely be incorporated into credit scoring. This could include utility bill payments (electricity, internet), mobile phone usage data, and even social media activity (with consent). This is particularly beneficial for the “credit invisible” population.

- AI and Machine Learning: Advanced algorithms will lead to more sophisticated and predictive credit scoring models, allowing for more precise risk assessment.

- Digital Identity Integration: Further integration of NIN and BVN will streamline identity verification and ensure more comprehensive credit profiles.

- Financial Inclusion: Improved credit scoring models will enable more Nigerians, especially those in rural areas or with informal incomes, to access formal credit, driving financial inclusion.

- Open Banking: The ongoing development of open banking frameworks in Nigeria could allow for more seamless sharing of financial data (with consumer consent), leading to richer credit profiles and more tailored financial products.

Recent economic developments, such as S&P Global Ratings upgrading Nigeria’s sovereign credit ratings to ‘B’ from ‘B-‘ on 15/05/2026, signal a stronger economic outlook. This, combined with increasing private sector credit (which rose to ₦94.6 trillion in January 2026), suggests a more robust and active credit market, making your personal credit score even more critical.

Frequently Asked Questions (FAQs)

Q1: How long does negative information stay on my credit report in Nigeria?

A1: Negative information, such as late payments or defaults, typically remains on your credit report for 3 to 5 years from the date of the last activity or settlement, depending on the specific type of negative mark and the bureau’s policy.

Q2: Can I get a loan if I have no credit history (a “thin file”)?

A2: It can be challenging, but not impossible. You might need to start with smaller loans from microfinance institutions or fintech lenders that specialize in new borrowers. Consistently repaying these small loans will help you build a positive credit history. Some lenders also consider alternative data like utility payments.

Q3: What’s the difference between a hard inquiry and a soft inquiry?

A3: A hard inquiry occurs when a lender checks your credit report because you’ve applied for new credit. It can temporarily lower your score. A soft inquiry happens when you check your own credit report or when a lender pre-approves you for an offer. Soft inquiries do not affect your credit score.

Q4: How often should I check my credit report?

A4: You should check your free annual report from each of the three bureaus (CRC, FirstCentral, CreditRegistry) at least once a year. This means you could potentially check a different bureau every four months for free. More frequent checks (paid) are advisable if you’re actively trying to improve your score or are planning a major loan application.

Q5: What should I do if I find an error on my credit report?

A5: Contact the credit bureau immediately. You’ll typically need to submit a dispute form and provide any supporting documents (e.g., proof of payment). The bureau is legally required to investigate and correct valid errors within a specific timeframe, usually 30 days.

Q6: Does my bank account balance affect my credit score?

A6: Your bank account balance itself doesn’t directly affect your credit score. However, consistent overdrafts or bounced cheques can be reported to the credit bureaus as negative financial behaviour, which could indirectly impact your perceived creditworthiness.

Q7: Can my credit score affect my employment chances in Nigeria?

A7: While not as common as in some Western countries, some employers, particularly in sensitive financial roles, may conduct credit checks as part of their background verification. This is usually done with your consent. A poor credit history might raise concerns about your financial responsibility.